In October, financial markets anticipated a single interest rate cut of 0.25% by the end of 2024. Surprisingly, by last week's close, the market sentiment shifted, and investors were now expecting five rate cuts. In response to these evolving market conditions, Knight Frank has released updated price forecasts for various UK regions.

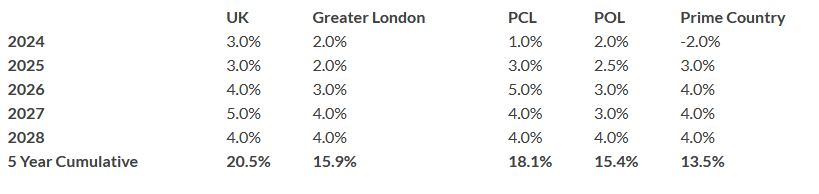

UK Sales Market Forecast

Tom Bill, Head of UK Residential Research at Knight Frank, attributes the revised outlook to a faster-than-expected decline in inflation. This shift recently prompted mortgage lenders to significantly lower their rates, seizing opportunities in a low-volume market.

The current landscape allows for a sub-4% best five-year fixed-rate mortgage, achievable after a one-percentage-point drop in the five-year swap rate during the final quarter of 2023. Consequently, Knight Frank has adjusted its UK house price forecasts, projecting a 3% increase in mainstream prices for 2024. This contrasts with the 4% decline predicted in October. Anticipating low-level single-digit growth in the following years, cumulative growth of 20.5% is expected by 2028.

Data from Halifax and Nationwide indicates a turning point, with a 1.7% increase and a 1.8% fall in 2023, respectively, compared to a previous 5% decline identified in August. Housing transactions in the UK, currently one-fifth below their five-year average, have prompted a cautious approach, waiting for a clear pattern signalling the bottoming out of prices, which is now believed to be the case.

Strengthened demand is reflected in a 10% year-on-year increase in mortgage approvals for November, with an anticipated double-digit percentage rise in sales volumes this year compared to 2023. The revised forecast for the mainstream London market projects a modest 2% growth, while lower-value areas are expected to outperform due to continued affordability constraints in the capital.

In the prime country house market, a narrower decline of 2% is forecasted for this year as the market adjusts from the highs experienced during the pandemic. Realistic asking prices become crucial as the 'race for space' no longer drives demand. Prime London markets may see more positive growth, albeit with higher risks due to the general election.

The prime central London (PCL) and prime outer London (POL) markets are expected to underperform the broader UK market this year, with the anticipation of more robust growth from the following year onward.

The article highlights that forecasts pertain to average prices in the existing homes market, and new build prices may not follow the same trajectory.

The momentum in the housing market's continuation is contingent on factors such as the timing of the general election. Potential risks include ideological divides within the ruling party and the ongoing conflict in the Red Sea, with potential implications for higher UK inflation. On a positive note, pre-election giveaways in the March Budget, including tax cuts and measures to assist first-time buyers, could further boost activity.

While a Labour victory is likely, proposed measures, such as overhauling the non-dom tax regime, increasing the stamp duty surcharge for overseas buyers, adding VAT to school fees, and altering inheritance tax rules, could impact demand in prime property markets.

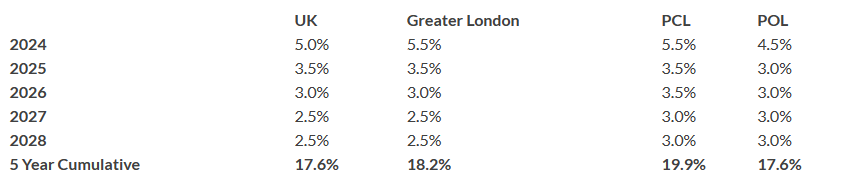

UK Rental Market Forecasts

Tom Bill from Knight Frank notes that landlords have been exiting the sector in recent years due to increased red tape and taxes, which have placed upward pressure on rental values. However, as supply recovers and more sellers become landlords in a sluggish sales market, the rental market dynamics are evolving.

According to Rightmove data, new listings in prime central London (PCL) and prime outer London (POL) were only 7% below the five-year average in December. Knight Frank has maintained its rental forecasts, projecting a 5.5% rental value growth in PCL and a 4.5% increase in POL for the current year.

Rental value growth is expected to be stronger in lower-value markets due to more significant supply/demand distortions. In contrast, higher-value markets have seen property owners being more discretionary, letting their properties while price growth has been flat.

The data indicates a notable difference in demand, with 4.3 new prospective tenants for every rental listing below £1,000 per week in PCL and POL, compared to 2.7 above £1,000 per week in the final quarter of last year.

Despite these trends, rising mortgage costs, taxes, and red tape are anticipated to maintain upward pressure on rents this year, keeping supply in check. The article mentions that Knight Frank's forecast of 5.5% rental value growth in PCL this year was last surpassed in 2011, excluding the distortive impact of the pandemic.

Across the UK, the Office for National Statistics (ONS) reported a record-high annual growth of 6.2% in November, reflecting supply-demand challenges in the broader rental market. As these challenges gradually ease, Knight Frank expects UK rental value growth to decline slightly to 5% this year, with London experiencing a slightly higher figure of 6% due to more robust demand.

Share:

-

-

-

Popular Blogs

-

.jpg?length=100&name=Email%20(25).jpg) Rising Foreign Ownership: Why Overseas Investors Are Turning to UK Property

Rising Foreign Ownership: Why Overseas Investors Are Turning to UK Property

-

London's Most Expensive Residential Postcodes: Where Are They?

London's Most Expensive Residential Postcodes: Where Are They?

-

.png?length=100&name=Email%20(28).png) UK Student Accommodation Booms as 2025 Investment Surges

UK Student Accommodation Booms as 2025 Investment Surges

-

.png?length=100&name=Email%20(50).png) 2025 Report: Gulf Investors Own the Most London Real Estate

2025 Report: Gulf Investors Own the Most London Real Estate

-

.png?length=100&name=Email%20(61).png) UK Property Market 2026: The Big Shift Begins — And the Smart Money Is Moving North

UK Property Market 2026: The Big Shift Begins — And the Smart Money Is Moving North

-

.jpg?length=100&name=Email%20(23).jpg) Interest Rates Could Drop to 2.5% by 2027: What It Means for UK Property Investors

Interest Rates Could Drop to 2.5% by 2027: What It Means for UK Property Investors

-

Why UK Property Investment is Thriving: 7.4% Average Yield in Q1 2025

Why UK Property Investment is Thriving: 7.4% Average Yield in Q1 2025

-

.png?length=100&name=Email%20(45).png) UK House Price Growth 2015–2025: What Overseas Investors Should Know

UK House Price Growth 2015–2025: What Overseas Investors Should Know

-

The Foreign Location with the Most UK Property Owners Revealed

The Foreign Location with the Most UK Property Owners Revealed

-

.png?length=100&name=Email%20(49).png) UK Real Estate Outlook to 2030: Resilience, Yields, and Long-Term Growth

UK Real Estate Outlook to 2030: Resilience, Yields, and Long-Term Growth

Related Articles

Knight Frank Revises Growth Forecast - UK rents to increase 23.9%

In a recent update, Knight Frank, a renowned lettings agency and property consultancy, has revised...Strong Demand in Prime London Property Market: Knight Frank Reports

According to the latest sales report by Knight Frank, the demand in the prime London property...